Explore Harvard Law News

The revolutionary history of American money

As the United States marks its 250th anniversary, Harvard Law Professor Christine Desan tells the origin story of U.S. currency and the Federal Reserve

Jun 26, 2026

By Scott Young

The power to make money and oversee its exchange is one of the most significant authorities wielded by government.

In the United States, this power lies with the Congress and a national banking institution it deputized to modulate the flow of government-backed currency known as the Federal Reserve. But from where did that power originate and, throughout the past 250 years, how has it changed?

According to Christine Desan, the Leo Gottlieb Professor of Law at Harvard Law School, the legislative power to make money pre-dates the signing of the Declaration of Independence. It also represents a hard-fought victory for the American colonies and a key factor in the decision to revolt against England.

“The hijacking of royal power started around 1690 in Massachusetts,” said Desan. “The Massachusetts legislature began spending its own IOUs into circulation and then taxing them back, giving them much more leeway to act outside the dictates of imperial officials. That’s how the whole center of power moved from royal governors to the colonial legislatures.”

In a conversation with Harvard Law Today, Desan explained the complex and fascinating history of the moneymaking power: its early beginnings, its evolution, and its direct link to American democracy.

HLT: Who has the power to make money? Where does the power to make money come from?

Desan: It depends on the way a society’s governed. But, broadly, money comes from the center of a community; that is, the stakeholders and folks with authority in the society. That could be a king or a monarch or a warlord. It could also be, in a democracy, a legislature. In the British and American cases I’ve studied, the struggle over the centuries was to move the power to make money from the monarch or the executive to the legislature as the more immediate representatives of the people. So, making democracy really consisted of getting control of the power to create money.

HLT: Why is it so important for the people or the legislature to have power over moneymaking?

Desan: We’re very used to thinking about “the power of the purse,” an authority that ensures that our legislative representatives and democratic officials have the power to spend and tax. That’s because we want them to direct the way resources move and we want only them — not autocrats or kings — to be able to obligate us. But we don’t often ask what, exactly, are they spending and taxing? Money, obviously. But that means that the power to make money comes first. There has to be something that the representatives are spending and taxing. If that something is made by a king, then the power to spend and tax is meaningless. If the monarch can make money him or herself and spend it him or herself, then the control over spending is illusory and the control over taxing becomes just a burden.

HLT: How did this struggle to control moneymaking affect the early American colonies?

Desan: In early America, the British monarch and his royal governors controlled spending and the legislatures were responsible for taxing. So, legislatures had the burden and did all the dirty work, while the royal governors distributed the resources. American legislatures came to power when they realized that they could invent their own form of money and control it. The colonial assemblies literally started spending provincial IOUs into circulation and then taxing them back in, creating a currency that people used in everyday exchange. In effect, the colonial legislatures created parallel economies that ran on the moneys the legislatures spent and taxed in; that activity marginalized the work that Crown officials were doing. When the American legislatures started spending and taxing, of course, they attracted all the attention of their constituents. As a result, the settlers started turning to the assemblies as the important location of governance because those assemblies were distributing resources and then obligating people by taxes to contribute. The moneymaking power is, understandably, a strong motivator for getting people actively engaged in civics.

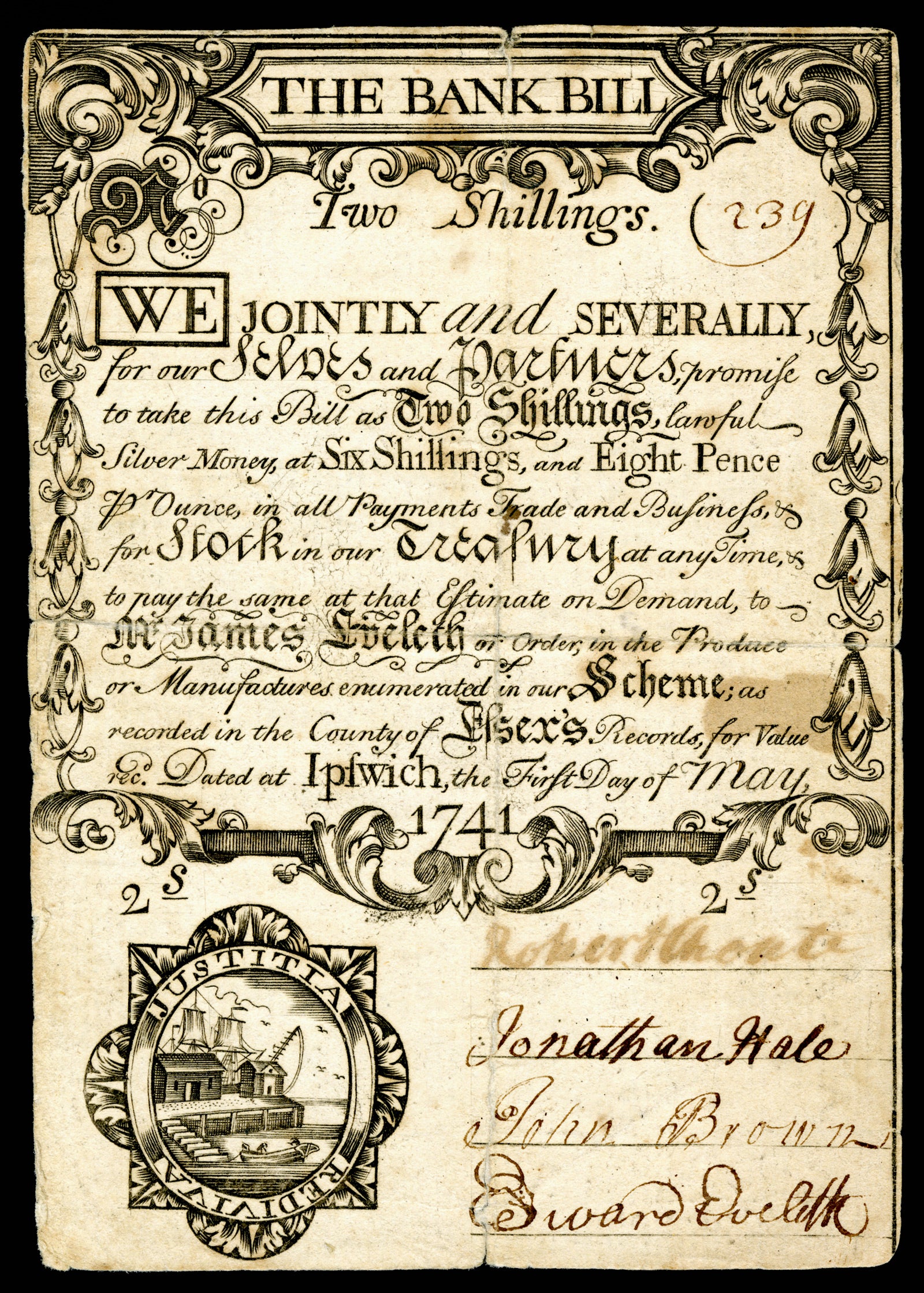

HLT: When did American money begin? How did these parallel economies emerge?

Desan: The hijacking of royal power started around 1690 in Massachusetts. The Massachusetts legislature began spending its own IOUs into circulation and then taxing them back, giving them much more leeway to act outside the dictates of imperial officials. Those authorities had ordered the Massachusetts population to send the militia to Quebec to fight the French and Native Americans there. The plan was that the soldiers would be paid with the spoils of victory. Well, they lost. So, the militia came straggling back to Beacon Hill — which, at that time, was just a hill with a tree — and they wanted to be paid. The legislators had nothing to give them, so they gave them literal IOUs that said, “This piece of paper is good on your taxes.” They couldn’t think of anything else to pay them with. But just consider — if everyone else had to pay their taxes in silver and gold coin and those soldiers could pay these IOUs, then the IOUs were essentially as good as silver and gold coin. The strategy worked, and the system took off. From then on, one colony after another started using this method and other methods of getting IOUs into circulation and then taxing them back in. They basically displaced the imperial governors in that moment.

HLT: How did American legislatures view the IOU-based economy and does that mindset remain in some form today?

Desan: Some pamphlets and other commentary from the time suggest that the colonial system made reciprocity in the community quite transparent. The public delivered defense, civil support, and some other benefits in return for contributions from their members and money came out of that reciprocal loop. The same logic holds today. Governments make money by spending to particular people in their IOU, in a public credit, and then taking back that IOU when it’s time for people to make their contribution. From that vantage point, they can direct spending, organize taxing, etc. It’s really empowering for a community to do that.

The dollar today is a still sovereign liability, it’s a credit. See 12 U.S.C. Section 411. But from those early days in the provincial assemblies, to the constitutional moment, to the Civil War, to the Federal Reserve, to the New Deal — each initiative is a change in the design of the way the American government is creating a monetary credit and putting it in circulation. Part of what’s important for us as lawyers to remember is that credit is a legal relationship. Credit can be issued, managed, and even multiplied in different ways. Once you see money as this form of credit, you can then open up its design and look at how it changed over time. That’s all that’s happened.

HLT: How did the framers of the U.S. Constitution feel about the moneymaking power?

Desan: First, the American Revolution occurs in part because the British tried to cut back on American legislative power. They literally enacted several parliamentary statutes to stop Americans from making their own paper currency, which helped catalyze resistance. After the Revolution, there are a set of nationally-oriented Americans — the framers — who understand that if they write a constitution leaving the moneymaking power with the states, then the states will be more powerful than the national government. So, instead, they put the moneymaking power clearly within congressional control. If we look at the U.S. Constitution, Article I, Section 8 — basically the first substantive section about legislative powers — it leads with the authorities to collect taxes, borrow, pay debts, regulate commerce, and coin money. The moneymaking powers all end up front and center. Most early national legislators probably assumed that coin would suffice as the main form of money in the New Republic. While it looks quite different, coin is actually another form of sovereign credit, one that carries collateral in the form of silver and gold. But Congress also early established the Bank of the United States. That’s an important design change in the way to make money.

HLT: What changed with the creation of the Bank of the United States?

Desan: When they established the Bank of United States, Congress delegated its moneymaking power to a third party, a set of investors, and allowed them to issue bank credit under certain conditions. In the legislation that set up the Bank of the United States, Congress actually provided that the United States would take that bank credit — in the form of bank notes, or liabilities — for taxes. So, if we look at the structure, it’s actually replicating the structure of endorsing a credit medium by taking it back for taxes. At the same time, it’s setting up a third party to which it can assign its own money-creative power. That is useful to Congress for a number of reasons. Silver and gold coin are very scant at that time. By contrast, the Bank of the United States, under the conditions Congress provides in the legislation, can amplify the money supply by creating more money in the form of bank notes. The Bank of the United States can also lend to individuals — again, under conditions that Congress recognizes. So, money borrowed by individuals in bank credit under the conditions that Congress specifies also becomes an important stream of money flowing into circulation. In addition, the new design also supports the national public debt, which furnishes the backing for the bank credit issued to the federal government. Finally, Congress is here creating a powerful alliance with financial elites. Money will enter circulation according to their judgment. That privilege will make banking a lucrative industry. As we’ll see, retail commercial banking becomes widely established at the state and then national level. Under the system, bankers acting for their own profit will determine how new money enters circulation. That channels funding to many productive ends because bankers lend to those borrowers they believe will succeed. At the same time, the method creates real distributive injustices because many worthy borrowers will not get financed. Women, Black Americans, union-shop employers, and many other projects that would enhance social welfare are shorted.

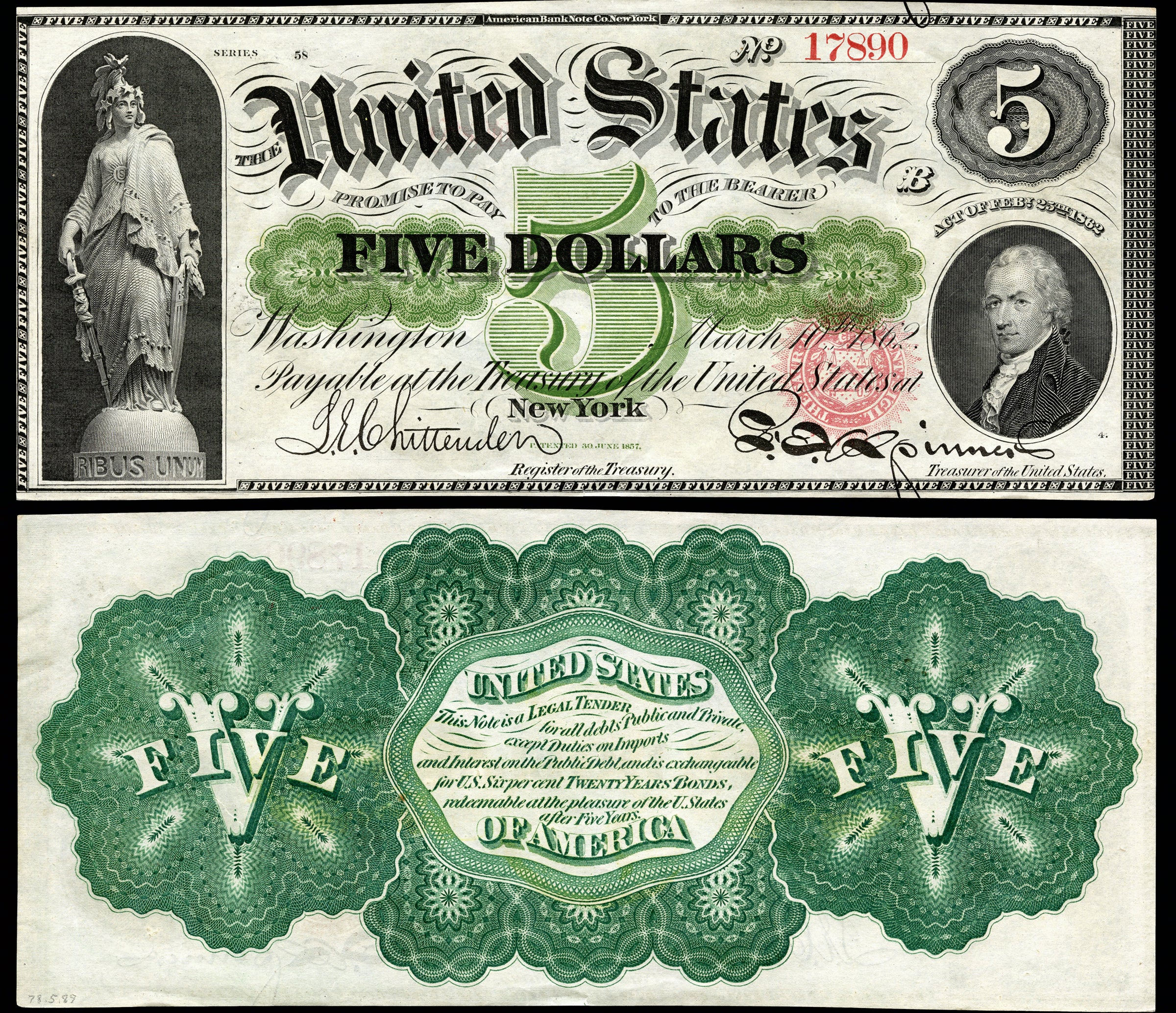

Congress, soon joined by the states, really experiments throughout the 19th century with different ways of making a money supply. One method is directly issuing IOUs, the most famous example of which is the greenbacks during the Civil War.

HLT: Why did Congress start issuing greenbacks during the Civil War?

Desan: Between the early Republic and the Civil War, Congress allows the states to move into the money creation territory. States do that by chartering their own banks and allowing those banks issue bank notes or deposit liabilities — both are promises-to-pay coin — under the conditions that are in the charter. That credit circulates and does a lot of the work of money, and the states support those state-chartered banks in a variety of ways, like taking their notes and using them for public payments. The states essentially created little sub-economies with their state currencies. It’s a bit reminiscent of the colonial period, although the federal dollar remains the unit of account. It’s a very interesting period that lasts from the early 19th century to the Civil War.

During the Civil War, the federal government moves back into that space, reacting against having allowed the state legislatures to compete with Congress. In 1860, the federal government finds itself with very little money in the in the U.S. treasury. There is no Bank of the United States because the charter of the second bank had expired and was not renewed. So, Congress uses the old colonial technique of issuing money into circulation: the greenback, which is just a simple IOU that the Union uses to pay soldiers and suppliers, allows to circulate as legal tender, and takes back for taxes. That IOU holds as long as the government taxes and runs the economy soundly, which the Union states manage pretty well given wartime. Inflation in the Union is comparable to the inflation that occurred during World War I. So, the greenback ends up being a very direct form of money creation.

HLT: How does the Federal Reserve eventually emerge out of this system?

Desan: During the Civil War, Congress sets up a national banking system that uses a lot of the infrastructure and practices that had been developed by the state-chartered banks. The national banks issue their own notes (or deposit liabilities) against national debt. Again, these are promises-to-pay the legal tender, i.e., greenbacks and, eventually, coin, that operate de facto as money. Congress is taking back those promises-to-pay, often in taxes, and using them to pay off the national debt.

The next big development is the Federal Reserve. The national banking system has a number of problems. First, there is a ceiling on how much money can be issued because Congress has set its conditions quite restrictively. It’s also regionally unbalanced with very few national banks in the south, which exacerbates existing problems when there’s seasonal demand for currency. Finally, there’s no institution that can modulate the pace at which the banks produce monetary credit. As a result, there are a number of financial crises in the decades after the Civil War. The final crisis in 1907 pushes Congress to establish the [Federal Reserve], an institution to coordinate the activities of the national banks, lend to them when they need more money, and tighten the credit system when they don’t. The Fed becomes the lender of last resort, the clearinghouse for banks to set off the mutual obligations they produce in the figure of their promises-to-pay, and the actor that will manage the pace at which monetary credit issues. Those powers are all based on the Fed’s ability to make money — its own ability to issue sovereign liabilities against certain assets within conditions established by Congress.

HLT: How would you characterize the complexity and efficacy of the existing system?

Desan: It’s an amazing system and it’s certainly complicated. On the other hand, it’s not really rocket science. The way the system works is very mechanical. We’ve tried different ways of creating sovereign money — thus the federal dollar that, as a circulating credit, allows us to measure and mobilize resources. In turn, we’ve tried different ways to multiply that unit of account, thus the retail commercial banks that advance their own credit for private use. Part of the role of money is to support the government. The government is still the single biggest spender in our economy, so, we need to empower the government. But all the rest of the approximately 80 percent of spending is by individuals who are using retail bank credit as money. They’re also in need of an instrument that will capture value and allow them to make transfers and exchanges.

The challenge is both to create a monetary flow in and out for the government and amplify that stream in ways that reach individuals and allow them to make their own exchanges. The Fed acts as a national bank at the center, creating the money that is the government’s ultimate sovereign liability. Then the commercial banks, the local banks, are out there like satellites. Ultimately, the monetary system is a fascinating and crucial engineering challenge. It needs to reach and irrigate all these different kinds of economic activity. And it needs to keep the money supply flowing in ways that are fair and equitable and stable. That challenge has required a lot of experimentation, elaboration, and revision over time. We are not finished yet — the modern system has irrigated much economic productivity. At the same time, it’s created many of the deep disparities we experience. We’ve got more essential work to do creating a just monetary system.

Want to stay up to date with Harvard Law Today? Sign up for our weekly newsletter.